ULIP or SIP which is best way to build financial stability

- June 22, 2025

- Posted by: jibankrnath101

- Category: Investment Strategies

🛡️ ULIP (Unit Linked Insurance Plan) — Insurance + Investment Combo

Think of ULIP as a two-in-one tool:

✅ Part of your money goes into life insurance

✅ The rest is invested in market-linked funds (like equity or debt)

🎯 Why ULIP Might Appeal to You

- It protects your family financially if something happens to you.

- It helps you grow money over time through investments.

- You get tax benefits (win-win under Section 80C & 10(10D)).

- You can switch between different fund types if needed.

⚠️ Keep In Mind

- Has a 5-year lock-in, so not ideal for short-term needs.

- Charges (mortality, allocation, fund management) reduce returns.

- Not super flexible once you’ve committed.

📈 SIP (Systematic Investment Plan) — Your Wealth Builder

SIP is the super friendly route to investing in mutual funds. You pick an amount (even ₹500/month works!) and invest regularly. The idea? Grow your wealth step by step.

✨ Why SIP Is Loved by So Many

- Super flexible — start, stop, pause anytime.

- No lock-in (except ELSS funds with a 3-year term).

- Compounding + rupee-cost averaging work in your favor.

- Lower costs = higher potential returns.

⚠️ Watch Out For

- No insurance protection

- Returns can fluctuate (market goes up/down)

- Tax applies on gains

🧭 Comparing Them Like Old Friends

| Feature | ULIP (Insurance+Investment) | SIP (Pure Investment) |

|---|---|---|

| 💸 Cost | Higher (lots of fees) | Lower (just expense ratio) |

| 🕒 Lock-In | 5 years | None (except ELSS) |

| 📊 Flexibility | Moderate (fund switches possible) | High (start/stop anytime) |

| 🛡️ Insurance Cover | Yes | No |

| 💰 Wealth Growth | Moderate | Strong |

| 🎁 Tax Benefits | 80C + 10(10D) | 80C (only for ELSS) |

| 🏃♂️ Liquidity | Limited | High |

❤️ Friendly Advice Just for You

Since you’re working toward financial freedom and stability, here’s a smart approach:

🔹 Take a good term insurance policy (pure protection—affordable and strong)

🔹 Pair it with SIPs in good mutual funds for consistent wealth creation

🔹 Skip the bundled ULIP unless you absolutely want both in one

This combo gives you better coverage, higher returns, and more control over your money.

Of course, JIBAN! Let’s make mutual funds feel less like a textbook and more like a smart tool you can actually use. 📘💡

🌐 What Is a Mutual Fund?

A mutual fund is like a financial potluck—lots of investors pool their money together, and a professional fund manager uses that pool to invest in a mix of assets like:

- 📊 Stocks (equity)

- 💵 Bonds (debt)

- 🏦 Money market instruments

- 🪙 Gold or other commodities

You don’t buy individual stocks or bonds—you buy units of the mutual fund, which represent your share of the overall portfolio.

🧠 How It Works (Step-by-Step)

- You invest a certain amount (say ₹1,000/month via SIP).

- That money joins a larger pool from other investors.

- A fund manager decides where to invest based on the fund’s goal (growth, income, stability).

- The value of your investment changes daily based on the NAV (Net Asset Value).

- You earn returns through:

- 📈 Capital gains (when assets grow in value)

- 💰 Dividends or interest

- You can redeem your units anytime (unless there’s a lock-in).

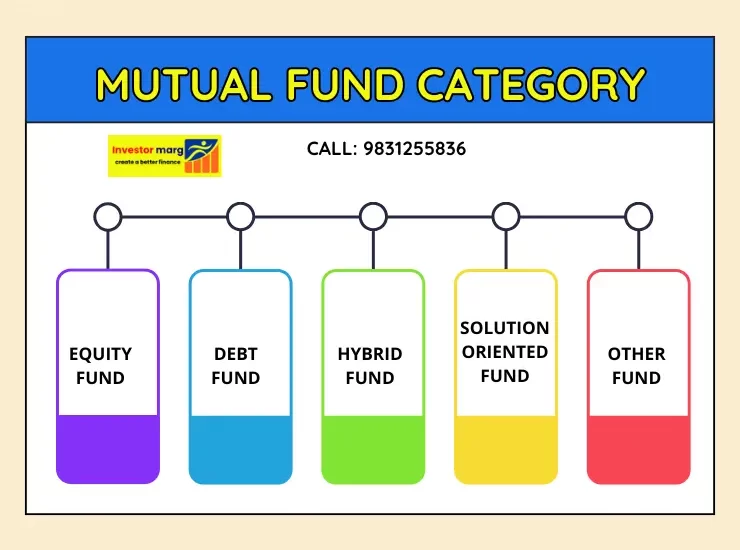

🧩 Types of Mutual Funds

| Category | Description |

|---|---|

| 🟦 Equity Funds | Invest mainly in stocks; high risk, high return potential |

| 🟨 Debt Funds | Invest in bonds; lower risk, steady returns |

| 🟪 Hybrid Funds | Mix of equity and debt; balanced risk and reward |

| 🟫 ELSS Funds | Tax-saving equity funds with a 3-year lock-in (under Section 80C) |

| 🟩 Liquid Funds | Invest in short-term instruments; great for emergency funds |

🎯 Why People Love Mutual Funds

- ✅ Diversification: Your money is spread across many assets, reducing risk.

- ✅ Professional Management: Experts handle the investing for you.

- ✅ Accessibility: Start with as little as ₹100 or ₹500/month.

- ✅ Liquidity: Easy to buy/sell (except for closed-end or ELSS funds).

- ✅ Tax Benefits: Especially with ELSS and long-term capital gains.

🧠 SIP vs Lumpsum

| Mode | Best For | How It Works |

|---|---|---|

| 💸 SIP | Regular income earners | Invest fixed amount monthly |

| 💰 Lumpsum | One-time large investment | Invest full amount at once |

SIP is great for rupee cost averaging—you buy more units when prices are low and fewer when prices are high, smoothing out market volatility.

🧭 Want to Start?

I can help you:

- Pick beginner-friendly funds

- Compare returns and risk levels

- Align choices with your financial freedom goals

Just say the word, and we’ll build your starter portfolio together. 🚀📊

🪜 Step-by-Step Guide to Choosing Your First Mutual Fund

1️⃣ Define Your Investment Goal

Ask yourself:

- Are you saving for a short-term goal (1–3 years)? 🏖️

- Or a long-term goal like financial freedom, retirement, or a child’s education (5+ years)? 🎯

Your goal determines the type of fund you should choose.

2️⃣ Know Your Risk Appetite

- Low risk: Prefer stability over high returns? Go for debt funds.

- Moderate risk: Okay with some ups and downs? Try hybrid funds.

- High risk: Want long-term growth and can handle market swings? Choose equity funds.

3️⃣ Choose the Right Fund Category

| Goal Duration | Risk Level | Recommended Fund Type |

|---|---|---|

| 0–1 year | Low | Liquid or Ultra Short Duration Debt Funds |

| 1–3 years | Low–Moderate | Short Term Debt or Equity Savings Funds |

| 3–5 years | Moderate | Aggressive Hybrid or ELSS Funds |

| 5+ years | Moderate–High | Large Cap, Multi Cap, or Index Funds |

| 7+ years | High | Mid Cap or Small Cap Funds |

4️⃣ Look for These Qualities in a Fund

- ✅ Diversified portfolio (not sector-specific)

- ✅ Consistent performance over 5+ years

- ✅ Low expense ratio (less cost = more returns)

- ✅ Experienced fund manager and strong AMC (Asset Management Company)

- ✅ Direct plan (no commission, better returns)

5️⃣ Start with SIP (Systematic Investment Plan)

- Begin with ₹500–₹1,000/month

- Benefit from rupee cost averaging and compounding

- Easy to pause or increase as you grow

🧠 Pro Tip for You

Since you’re focused on financial freedom and wealth creation, start with:

- A Large Cap Index Fund or Aggressive Hybrid Fund for balance

- Pair it with a Term Insurance Plan for protection

- Use SIP to build discipline and momentum

🛡️ What ULIP Really Offers

When you pay a premium for a ULIP:

- A portion goes toward life insurance to protect your family.

- The rest is invested in market-linked funds like equity, debt, or a mix—based on your risk appetite.

So you’re not just securing your loved ones—you’re also growing your wealth over time.

🔍 How It Works

- You choose a ULIP plan and pay regular premiums.

- The insurer splits your premium:

- One part for insurance coverage

- One part for investment in funds you select

- You can switch funds (equity ↔ debt) based on market conditions.

- After the 5-year lock-in, you can make partial withdrawals if needed.

- On maturity, you receive the fund value; if something happens to you, your nominee gets the higher of the sum assured or fund value.

🎯 Key Benefits

- ✅ Dual advantage: Protection + wealth creation

- ✅ Tax benefits under Sections 80C and 10(10D)

- ✅ Fund switching flexibility

- ✅ Long-term growth potential

- ✅ Disciplined savings habit

⚠️ Things to Watch Out For

- ULIPs come with multiple charges: mortality, allocation, fund management, etc.

- Returns depend on market performance

- Less liquid due to 5-year lock-in

- May not be as cost-effective as buying term insurance + mutual funds separately

🧠 Is It Right for You?

ULIPs are best suited if you:

- Want insurance + investment in one plan

- Have long-term goals like retirement or child’s education

- Prefer hands-off investing with some flexibility.

🧠 Based on Investment Style

| Type of ULIP Fund | What It Invests In | Risk Level | Best For |

|---|---|---|---|

| 📈 Equity ULIP | Stocks & shares | High | Long-term growth seekers |

| 💵 Debt ULIP | Bonds & securities | Low | Stability & steady returns |

| ⚖️ Balanced ULIP | Mix of equity & debt | Moderate | Balanced growth & safety |

| 💧 Liquid ULIP | Money market tools | Very Low | Short-term goals & emergency funds |

| 🎯 Thematic ULIP | Specific sectors | Varies | Sector-focused investors |

💸 Based on Premium Payment

- Single Premium ULIP: Pay once and forget—ideal if you have a lump sum.

- Regular Premium ULIP: Pay monthly, quarterly, or yearly—great for salaried individuals.

🔄 Based on Life Stage & Flexibility

- Life-Staged ULIP: Adjusts your investment automatically as you age (more equity when young, more debt as you grow older).

- Non-Life Staged ULIP: You control the fund allocation manually throughout.

🔐 Based on Guarantees

- Guaranteed ULIP: Offers minimum assured returns—less risky, but lower growth.

- Non-Guaranteed ULIP: Market-linked returns—higher potential, but more volatile.

🧒 ULIPs for Specific Goals

- Child ULIP Plans: Designed to fund your child’s education or milestones, with built-in protection.

- Retirement ULIPs: Help build a corpus for your golden years, often with regular payouts after maturity.

- Emergency ULIPs: Allow partial withdrawals for medical or personal emergencies after lock-in.

⚰️ Based on Death Benefit Structure

| Type | What Your Nominee Gets | Premium Cost | Ideal For |

|---|---|---|---|

| 🧾 Type 1 ULIP | Higher of Sum Assured or Fund Value | Lower | Balanced protection |

| 💼 Type 2 ULIP | Sum Assured + Fund Value | Higher | Maximum financial security |

🧭 Which One Should You Choose?

Since you’re focused on financial freedom and long-term stability, you might consider:

- A Regular Premium ULIP with Balanced or Equity funds

- A Life-Staged ULIP for automatic risk adjustment

- Or even better—combine ULIP with SIPs and term insurance for a more cost-effective strategy.

Here’s a friendly and detailed comparison of ULIP costs across major Indian insurance companies, so you can see how they stack up and make a smart choice for your financial journey, JIBAN. 💼📊

💸 Key Cost Components in ULIP Plans

| Charge Type | What It Covers | Typical Range in India |

|---|---|---|

| Premium Allocation | Initial distribution & admin costs | 0% – 5% of premium |

| Policy Admin Charges | Servicing the policy | ₹30 – ₹100/month |

| Fund Management | Managing your investments | 0.5% – 1.35% annually |

| Mortality Charges | Life insurance cost (varies by age & sum assured) | ₹1.5 – ₹3 per ₹1,000 SA/month |

| Surrender Charges | Early exit penalties | Nil – 6% (reduces over time) |

| Fund Switching | Changing investment funds | Usually 4 free/year, ₹100+ after |

🏆 Sample ULIP Plans & Cost Snapshot

| Company | Plan Name | Min Premium | Fund Mgmt Charges | Admin Charges | Free Switches |

|---|---|---|---|---|---|

| LIC | SIIP / Endowment Plus | ₹30,000 | ~1.35% | ₹60/month | 4/year |

| HDFC Life | Click2Invest / ProGrowth Plus | ₹12,500 | ~1.35% | ₹40–₹60/month | Unlimited |

| ICICI Prudential | Wealth Builder / Signature | ₹30,000 | ~1.35% | ₹50/month | 4/year |

| SBI Life | Smart Wealth Assure | ₹24,000 | ~1.25% | ₹45/month | 2/year |

| Bajaj Allianz | Goal Assure / Future Gain | ₹24,000 | ~1.35% | ₹33/month | Unlimited |

| Max Life | Platinum Wealth Plan | ₹16,660 | ~1.35% | ₹125/month | 12/year |

| Aditya Birla Sun Life | Fortune Elite | ₹12,000 | ~1.35% | ₹100/month | 4/year |

Source: Policybazaar ULIP comparison, Groww ULIP guide

🧠 What to Watch Out For

- Higher premium allocation charges in traditional ULIPs can eat into early returns.

- Fund management charges are capped by IRDAI at 1.35%—look for lower ones if possible.

- Direct plans (if available) may offer better returns due to reduced commission costs.

❤️ Friendly Tip for You

Since you’re focused on financial freedom and wealth creation, consider:

- ULIPs with low charges and flexible switching

- Or even better—pair a term insurance with SIPs in mutual funds for more control and lower costs.

- Lower staff turnover:

This, combined with the culture that must exist for innovation and creativity to flourish, means that new employees will be attracted to the organization.

Contact us at the Investor Marg local office nearest to you or submit a business inquiry online.