Proper Family Budgeting extra savings

- July 3, 2025

- Posted by: jibankrnath101

- Category: financial services

Proper Family Budgeting for Extra Savings

- Understand your total household income and list all sources clearly—this sets the foundation for realistic planning

- Categorize expenses into essentials (like food, rent, utilities), non-essentials (entertainment, dining out), and irregular costs (festivals, school fees)

- Allocate fixed percentages to each category using methods like the 50/30/20 rule to balance needs, wants, and savings

- Prioritize saving by treating it as a non-negotiable expense—automate transfers to savings or investment accounts

- Monitor spending habits regularly to identify areas where you can cut back without affecting quality of life

- Plan for emergencies by building a buffer fund that covers at least 3–6 months of essential expenses

- Involve all family members in budgeting discussions to encourage responsibility and teamwork

- Use budgeting tools or spreadsheets to track progress and adjust as life changes—like new goals or income shifts

- Redirect any surplus or unexpected income (bonuses, gifts) toward savings or debt repayment

- Review your budget monthly to stay aligned with financial goals and make improvements where needed

It starts with understanding where your money goes each month—everything from groceries and rent to subscriptions and leisure—then building a spending plan that protects necessities while supporting long-term goals. A well-managed budget brings clarity to needs versus wants, helping you control overspending and avoid debt traps.

Extra savings come not from big income leaps but from small, consistent choices. Smart budgeting sets aside a portion of income first—for emergencies, future investments, or family goals—before allocating expenses. It encourages comparing deals, cutting back on unused services, and making mindful purchases. Over time, these practices build a safety net and free you from the anxiety of living paycheck to paycheck. As priorities shift—like saving for a child’s education or planning retirement—the budget adapts to reflect those changes. It’s not just numbers on a spreadsheet, but a living system that helps your family thrive financially with purpose and peace.

Effective budgeting for families blends structure with flexibility, making sure everyone’s needs are met while building toward shared goals. Start by tracking all sources of income and categorizing expenses into essentials like housing, groceries, and utilities, versus discretionary spending like entertainment or dining out. This clarity helps identify areas to cut back without sacrificing quality of life.

Choosing a budgeting method that fits your lifestyle—like the 50/30/20 rule or zero-based budgeting—can simplify decision-making. Tools like Mint or YNAB make tracking easier and more visual, especially when synced with bank accounts. Involving the whole family, even kids in age-appropriate ways, fosters teamwork and financial literacy. Setting SMART goals—specific, measurable, achievable, relevant, and time-bound—keeps everyone motivated, whether it’s saving for a vacation or building an emergency fund.

Regular reviews are key. Life changes, and so should your budget. Adjust for new jobs, school fees, or unexpected expenses. Celebrate milestones to keep spirits high, and remember: budgeting isn’t about restriction—it’s about empowerment and peace of mind.

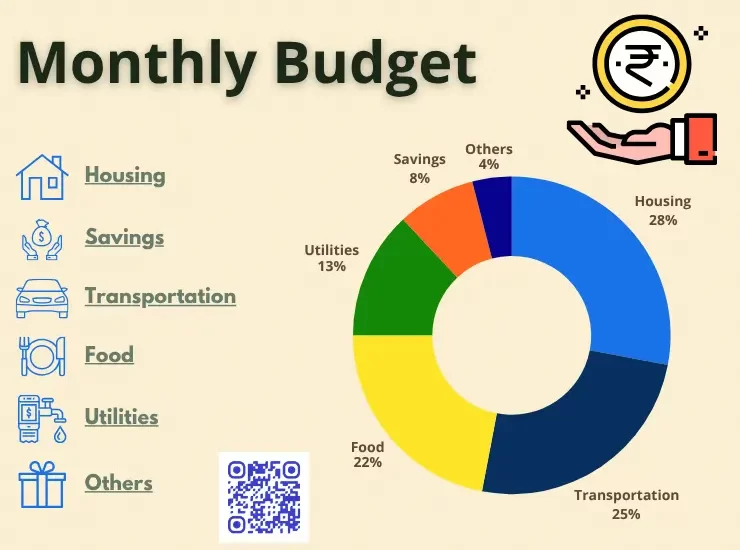

- Investment allocation 50/30/20 rule in detail?:

Absolutely! The 50/30/20 rule is a simple yet powerful budgeting framework that helps you manage your after-tax income by dividing it into three categories:

50% for Needs: These are essentials you must pay to live and work. Think rent or mortgage, groceries, utilities, transportation, insurance, and minimum debt payments. If this category exceeds 50%, it’s a signal to reassess lifestyle choices—maybe downsize housing or reduce commuting costs.

30% for Wants: This bucket covers non-essentials that enhance your lifestyle—dining out, entertainment, travel, shopping, subscriptions, and hobbies. It’s where you enjoy life, but with moderation. Being mindful here helps prevent overspending and frees up room for savings.

20% for Savings and Debt Repayment: This is your future-proofing fund. It includes building an emergency fund, investing for retirement, and making extra payments on loans. Ideally, you automate this portion so it’s consistent and grows over time.

For example, if your monthly income after tax is ₹60,000:

- ₹30,000 goes to needs

- ₹18,000 to wants

- ₹12,000 to savings and debt repayment

This rule is flexible—you can tweak the percentages based on your goals or cost of living. It’s especially helpful for families because it balances present comfort with long-term security. Want help customizing it to your situation or exploring alternatives like the 70/20/10 rule? I’ve got you covered.

- Proper Budgeting of expense avn be helpful for extra savings:

🧾 Track every rupee: Monitor all spending—big or small—to find hidden leaks like unused subscriptions or impulse buys.

🛒 Categorize your expenses: Divide costs into essentials (food, housing, transport), non-essentials (entertainment, dining out), and variable costs (gifts, medical bills). It helps you prioritize.

📊 Set spending limits: Put a cap on each category to prevent overspending and maintain control.

📅 Plan for irregular expenses: Set aside funds monthly for annual costs like insurance premiums, school fees, or festivals—so they don’t disrupt your budget.

💡 Automate savings first: Treat savings like a fixed expense—move it out as soon as income arrives, so you’re not tempted to spend it.

🔄 Review and adjust regularly: Life changes—new goals, new expenses. Revisit your budget monthly to stay aligned and improve.

🎯 Use budgeting apps or spreadsheets: Tools like Excel or apps like Walnut or Goodbudget give visual clarity and simplify tracking.

🪙 Turn savings into investments: Once extra funds accumulate, channel them into mutual funds, PPF, or ULIPs to multiply your wealth over time.

Would you like help building a sample budget sheet or exploring apps that make this easier? I can tailor it to your goals and income flow.

🎯 Define your goals clearly: Know what financial freedom looks like for you—whether it’s retiring early, traveling without worry, or securing your family’s future. Use SMART goals (Specific, Measurable, Achievable, Relevant, Time-bound) to give your vision structure.

📊 Track your current financial status: Understand your income, expenses, assets, and liabilities. This gives you a baseline and reveals areas to improve.

💸 Pay yourself first: Before spending, allocate a portion of your income to savings and investments. Automate this process so it becomes a habit.

🧾 Create and stick to a budget: Use tools or spreadsheets to monitor spending. Prioritize needs, limit wants, and redirect excess toward your goals.

🧨 Eliminate high-interest debt: Use strategies like the snowball or avalanche method to pay off loans. Debt is a major barrier to freedom.

📈 Invest wisely and consistently: Start early, diversify across assets (mutual funds, ULIPs, PPF, index funds), and use SIPs to build wealth gradually.

💼 Increase your income: Upskill, explore side hustles, or affiliate marketing (like Zepto, which you’re already exploring). Multiple income streams accelerate progress.

🛡️ Build an emergency fund: Aim for 3–6 months of expenses to protect against unexpected setbacks.

🔄 Review and adjust regularly: Life changes—so should your financial plan. Stay flexible and informed.

📚 Keep learning: Read books, take courses, and stay updated on financial trends. Knowledge is your greatest asset.How to get Financial Freedom?:

Achieving financial freedom means reaching a point where money no longer dictates your choices—it supports them. It’s not just about having wealth, but about having control, peace of mind, and the ability to live life on your terms. Here’s how you can work toward it

- Extra Money saving Tips:

Sure, JIBAN! Here’s a more relaxed and friendly take on extra money-saving tips, just in bullet points:

- Track your daily spending to understand where your money goes and spot areas to cut back

- Wait before buying non-essential items—often you’ll realize you don’t need them

- Choose store brands over name brands to save without sacrificing quality

- Cook meals at home and plan your weekly menu to avoid food waste and expensive takeout

- Review your subscriptions and cancel the ones you rarely use

- Use apps that offer cashback or rewards when you shop or pay bills

- Set up automatic transfers to savings right after payday so you don’t forget

- Sell unused items online or locally to declutter and earn extra cash

- Call service providers to negotiate better rates on bills and insurance

- Make a shopping list and stick to it to avoid impulse purchases

Want me to help you build a personalized savings plan based on your current income and goals? Contact in whatsapp on +91 9831 255 836.

Contact us at the Investor Marg local office nearest to you or submit a business inquiry online.